Have you ever searched frantically for your keys only to discover you were holding them in your hand?

The same thing happens in investing: we fail to see opportunities that are right in front of us. Sometimes investors miss lucrative opportunities because they harbor false beliefs about a particular field or sector.

That’s happening right now in the energy sector. Many investors misunderstand the direction of the industry, and their confusion is creating a rare opportunity for others to invest in a large, undervalued market that’s positioned for growth.

Venture capitalists (VCs) love a product that

solves a painful problem

in a huge global market

that is ripe for technological disruption

and has high growth potential and undervalued companies.

The energy sector satisfies all of these conditions.

Energy companies need to solve a painful problem. Energy producers need to lower greenhouse gas emissions while keeping energy affordable. Governments, companies, and financial institutions are committing trillions of dollars to reduce climate risk, and corporations face stricter government regulations and pressure from investors to curb emissions.

In addition, the need for energy continues to rise. Energy is an enabling technology; it empowers people to get the other things they want–in fact, almost every other thing they want. Try going a day without your phone, hot water, lights, refrigerator, or car. Modern civilization grinds to a halt without access to affordable and reliable energy.

Energy is the largest market in the world. Nearly $2 trillion is spent on energy every year[1]—more than enterprise software,[2] fintech,[3] and consumer electronics[4] combined.

The energy sector is ripe for technological disruption. Over 60% of energy is wasted because of inefficiency in the current system.[5] Energy companies are desperate for new technology that drives down emissions and helps find, generate, move, and use energy efficiently, which is the key to making it more affordable.

The energy sector has high growth potential and undervalued companies. Global demand for energy is increasing now, and it will continue to increase in the future. Energy consumption more than doubled between 1971 and 2020,[6] and it’s projected to grow 50% by 2050.[7] Energy fuels all the benefits of modern life: healthcare, education, transportation, communication, and economic growth. Developed countries don’t want to give up those benefits, and developing countries want more of them. In addition, new technologies such as artificial intelligence and robotics require even more energy. As a result, the demand for energy will continue to increase in the future.

Finally, companies in the energy sector are some of the most undervalued. Fear of missing out is currently driving investors toward trending categories like the metaverse, artificial intelligence, and crypto. As a result, sectors like energy tech are undervalued.

Many investors assume solar, wind, and batteries are the most promising ways of achieving low-emission energy and implementing the preferred environmental, social, and governance framework (ESG). ESG is a legitimate concern: we want cleaner air and water, lower greenhouse gas emissions, and increased quality of life for people around the world.

However, solar and wind are not the best ways to implement ESG. They’re unreliable; they raise electricity rates and over-consume minerals and land.[8] In general, solar and wind don’t have the power density to fuel modern life. Even after $2.7 trillion has been invested in solar and wind over the last decade, they still produce only 3% of global energy.[9] So when solar and wind fail (and they will), people will be forced to turn to more cost-effective and reliable sources of power.

Contrary to what many energy investors think, the biggest winner in the energy sector in the next 10 years will be natural gas–especially technologies that enable the efficient production, transport, and use of natural gas.

Natural gas provides the most cost-effective near-term solution for affordable, reliable, low-emission energy. Shifts from coal to natural gas have produced the biggest emissions reductions over the past 15 years. Natural gas produces only 10% of the air pollutants and 50% of the CO2 that coal does.[10] Natural gas also has many uses beyond providing power; fertilizers, computers, medical equipment, steel, plastic, mobile phones, cars, and most consumer products are currently made from natural gas and oil. In fact, even solar and wind require natural gas as a backup because they don’t operate most of the time.

Energy Capital Ventures (ECV) is one of the few VCs that sees the potential of natural gas. Instead of chasing popular trends, ECV correctly sees the path to achieving low-emission energy will come through investments in scaleable energy technology such as advanced leak detection and methane capture, process automation and controls, renewable natural gas, and synthetic microbes that absorb greenhouse emissions.

Energy tech is similar to fintech 15 years ago. Just as fintech took off, energy tech will soon soar just as high. It’s rare to be positioned so well to capitalize on future growth. The keys are in your hand. Don’t miss out!

Liberty is a tech company disguised as an oilfield services firm. Technology innovations are helping the company increase production, lower costs, and enhance environmental, social, and governance (ESG) performance.

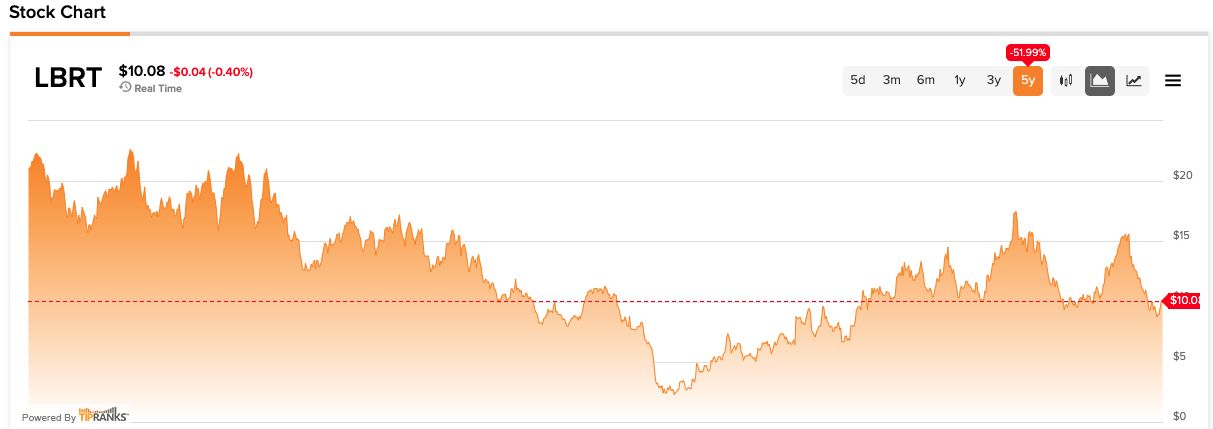

Liberty annual earnings are projected to grow nearly 80% over the next 3 years. Its stock price (US~$10) on 12/9/21 is ~15% undervalued.

Liberty has provided a 24% average cash return on capital invested over 9 years.

Liberty Oilfield Services (NYSE: LBRT) is undervalued and positioned for growth. Liberty offers fracking services to energy companies across North America. A method of extracting oil and natural gas, fracking involves drilling into the ground and applying fluids under high pressure to release the oil and gas contained in underground rock formations. But don’t be fooled by simplistic job descriptions. Liberty is actually a tech company disguised as an oilfield services firm.

Liberty’s outspoken CEO, Chris Wright, unapologetically highlights the critical role oil and gas play in pulling people out of poverty, reducing environmental harm, and fueling the benefits of modern life.

Wright first grabbed my attention when he made this video highlighting the hypocrisy of North Face, which makes high-quality outdoor recreation gear. North Face refused to make a co-branded jacket with one of Liberty’s competitors, an oil and gas company. Chris exposed this silly act of virtue-signaling by buying ad space on billboards near North Face’s headquarters to point out that their products are made with the help of the oil and gas industry.

Chris does not come from a traditional industry background. He’s a self-described “energy nerd” who studied mechanical and electrical engineering at MIT and UC Berkeley and worked on nuclear fusion. His first company, Pinnacle Technologies, helped launch commercial shale gas production in the late 1990s. Chris started Liberty in 2011, and in the past ten years, the company has grown to a $1.7 billion market capitalization and ~2,500 employees. Liberty, which had its IPO in 2017, is headquartered in Denver, Colorado.

Liberty’s technology advantage

Liberty’s technology portfolio includes ~500 patents and strategic acquisitions to raise productivity and lower costs, and it has helped customers reduce the cost to produce a barrel of oil by more than 65% over the last eight years, according to Liberty’s 2020 annual report. The company’s quest for increasing productivity delivers lower emissions and boosts environmental, social, and governance (ESG) performance.

Liberty’s data-rich ESG report is not the typical “we are less bad” report full of greenwashing, buzzwords, and empty promises. It looks instead at a bigger picture of our world and describes the positive impact Liberty and the industry make on energy access, healthcare, education, transportation, communication, and economic growth.

Here’s a sample of some of the technology innovations helping Liberty increase production, lower costs, and enhance ESG performance.

Liberty introduced “FracSense,” a diagnostic service to help customers acquire more accurate well data to optimize hydraulic fracture completions and well spacing.

Liberty set a record for a 24-hour period of continuous pumping using real-time data tracking, predictive analytics, and supply chain and logistics integration.

Liberty developed “Quiet Fleet” technology to reduce noise emissions during hydraulic fracturing operations by a factor of 3 compared to a conventional fracturing fleet.

Liberty acquired PropX, a provider of delivery equipment, logistics, and software solutions to drive efficiency and reduce noise and emissions.

Liberty acquired Schlumberger’s onshore hydraulic fracturing business in the United States and Canada including proprietary controls, novel software, and fleet automation.

Liberty is in the process of launching electric frac pumps with 40% more horsepower and 25% lower emissions than conventional technologies.

Outlook Liberty’s annual earnings are projected to grow nearly 80% over the next three years. And its current stock price (US~$10) is currently ~15% undervalued (on 12/9/21), according to stock market analysts.

Natural gas will be the biggest winner in the energy sector over the next decade. The demand for energy continues to outpace supply, as evidenced by the current energy crisis in Europe and China. Underinvestment in global oil and natural gas production has led to higher energy prices and shortages. Increasing demand, policies aimed at reducing climate risk, and current market incentives will likely make the supply shortage last through this decade because it’s clear we’re going to need a lot more energy than we’re generating now. Energy runs on a predictable cycle like other commodities, and we are at the beginning of a new cycle.

The world is moving to natural gas because it’s reliable, affordable, and emits fewer greenhouse gases than the alternatives. Contrary to what many investors think, the biggest greenhouse gas reductions over the past 15 years are not related to increased solar and wind power but to shifts away from coal and toward natural gas. (I explain more about this in another article.) Natural gas produces about half the carbon dioxide and just one-tenth of the air pollutants that coal does.

All of these conditions mean Liberty is well positioned for growth.

Risk analysis

ESG mandates and investor pressure are the greatest threats to the oil and natural gas industry. Many investors and politicians don’t understand the energy system and are confused by the myriad messages they’re hearing about renewable energy and climate risk. Concerns about climate risk have led to corporate and government incentives that channel money away from oil and gas production. These incentives may impact the cost of capital, which will put American oil and gas companies at a disadvantage. S&P Global Ratings estimates funding costs were about 75 basis points higher on average for the most carbon-intensive borrowers from the North American energy sector.

In addition, the U.S. oil and gas industry will likely face more regulation. In fact, the Environmental Protection Agency (EPA) announced new rules in November 2021 that strengthen regulations on new oil and gas wells. If a carbon tax is imposed in the future, it will negatively impact the value of U.S. oil and gas companies. President Biden’s orders to halt oil and natural gas leases on public lands and waters can also hurt U.S. industry. These efforts to curb planet-warming carbon emissions are counterproductive and may lead the U.S. to import energy from countries with less strict environmental regulations—something that will increase greenhouse gas emissions.

Although the regulatory efforts will be counterproductive, they can still negatively affect the U.S. oil and gas industry. In addition, geopolitics can have a huge impact on the supply and price of energy. Economic sanctions on energy-rich countries like Iran, Russia, and Venezuela can quickly move the global energy market up or down.

Liberty is not immune to macroeconomic forces like higher transportation costs, driver scarcity, and labor shortages caused by Covid-19.West Texas Intermediate (WTI) oil prices dropped as low as $18 per barrel in the spring of 2020, and supply chain disruptions, materials shortages, labor scarcity, and rising costs all eat away at margins.

Despite these risks to oil and gas companies, the truth is that solar and wind provide less than 3% of global energy after two decades and $2 trillion invested, including heavy subsidies. The world currently runs on 84% hydrocarbons. People are going to continue to need hydrocarbons to meet their energy needs for many decades, and unless Americans are going to give up air conditioning, heating, driving, computers, and flying in airplanes, we are going to continue to use oil and gas.

And as we are now exiting the historic Covid downturn, oil is near ~$70 per barrel and the supply chain and labor shortages will fade as the global economy bounces back.

Financial health

Liberty reported a third-quarter 2021 loss per share of 22 cents. The underperformance is due largely to expenses related to acquiring and integrating the onshore hydraulic fracturing business it purchased from Schlumberger in January.

Liberty had approximately $35 million in cash and cash equivalents as of September 30, 2021. Its long-term debt of $122 million represented a debt-to-capitalization of 9.2%. Further, the company’s liquidity—cash balance, plus revolving credit facility—amounted to $268 million.

Zoom out, and Liberty has provided a 24% average cash return on capital invested over 9 years

Investment recommendation

I’ve invested my own money in Liberty because I have high conviction in its future growth prospects. I’m a long-term investor and plan to hold my investments for at least three to five years.

Your ultimate goal as an investor is to buy assets for less than they are really worth, and Liberty currently provides that opportunity. The volatility of the energy market allows investors to reap large returns, but make sure you have the right constitution to weather large swings in stock price before you jump into this pool.

Be patient and wait for the right price. If you decide to invest, consider reducing the risk by buying your desired position in four tranches. Look to buy your first investment-sized tranche below $11/share. Liberty is a growth stock and does not pay a dividend.

Current stock price near historic lows

Key Takeaways

Liberty’s annual earnings are projected to grow nearly 80% over the next 3 years. Its current stock price (US~$10) is currently ~15% undervalued.

Liberty is a tech company disguised as an oilfield services firm. Technology innovations are helping the company increase production, lower costs, and enhance ESG performance.

Liberty has a strong founder/CEO with a proven track record.

Natural gas will be the biggest winner in the energy sector over the next decade. The world is moving to natural gas because it’s reliable, affordable, and emits fewer greenhouse gases than the alternatives.

Liberty is not immune to macroeconomic forces like higher transportation costs, driver scarcity, and labor shortages caused by Covid-19.

ESG concerns and investor pressure may impact the cost of capital, which would put American oil and gas companies at a disadvantage.

Liberty has provided a 24% average cash return on capital invested over 9 years.

My analysis is presented for general informational purposes and does not constitute investment advice. Do your own research. Individuals have unique circumstances, goals, and risk tolerances, so you should consult a certified investment professional and/or do your own due diligence before making investment decisions.

Natural gas and nuclear power will be the big winners in the energy sector over the next 20 years. They have a competitive advantage over solar, wind, hydro, geothermal, coal, and oil. That advantage, combined with market factors, sets up rare investment opportunities to hold high-quality energy companies and buy natural gas and uranium futures.

People in different parts of the world—from Sacramento to Frankfurt to Beijing—are currently experiencing higher energy prices and shortages. Three main factors are at work here:

Increased demand,

Policies aimed at reducing climate risk,

Current market incentives.

Global demand for energy is increasing. Energy fuels all the benefits of modern life: healthcare, education, transportation, communication, and economic growth. Developed countries don’t want to give up those benefits, and developing countries want more of them. As a result, the demand for energy will continue to increase over the next 20 years.

But supply isn’t currently increasing to meet that demand. Concerns about climate risk have led to corporate and government incentives that channel money away from oil and gas production toward solar and wind power, and environmental activists in Europe and the U.S. have successfully slowed the development of nuclear power. Investors lost money betting on the energy sector over the last decade, so the stock market has been rewarding energy companies for strengthening their balance sheets and returning cash to shareholders instead of investing in new long-term projects.

But things are poised to change. Energy runs on a predictable cycle like other commodities. As demand for energy increases, the price of energy also increases because supply is limited. Higher prices attract producers to invest in new production. New production kicks into overdrive because companies start competing to produce more. This competition leads in turn to oversupply: prices crash, and producers stop investing. Supply then gets tight; prices start rising again, and the boom-bust cycle continues.

We are at the beginning of a new cycle. The supply shortage we’re currently experiencing will likely last the remainder of this decade. Investors will find rare opportunities to capitalize on growth.

Global demand for energy is increasing

Energy is the lifeblood of modern civilization, the driving factor behind human progress and human flourishing. Our food, water, housing, transportation, communication, healthcare, and economic development all depend on harnessing energy.

Energy isn’t limited to generating electricity. It is needed for transportation, heating, and producing most of the materials and products we rely on: plastics, fertilizer, computers, medical equipment, mobile phones, cars, and airplanes–all currently made from oil and natural gas.

The world is hungry for energy. Global energy consumption more than doubled between 1971 and 2020,[1] and it’s projected to increase nearly 50% by 2050.[2] It’s clear that we’re going to need a lot more energy than we’re generating now. Some people believe that when we learn to harness new sources of energy, we will stop using our current sources. But that has never been true. Historically, whenever we learned to harness a new energy source, we did not stop using the sources we previously relied on (Figure 1).

Figure 1: Harnessing new energy sources did not replace energy sources we used before.

Future demand for energy isn’t going to be evenly distributed around the globe. Over 3 billion people—40% of the Earth’s population—currently live in energy poverty.[3] Most of the increased future demand for energy is going to come from providing these people with the energy they need and deserve. This is especially true in Asia where standards of living are rapidly increasing.

Navigating climate risk

Climate risk is a real problem because warming temperatures likely increase the severity of floods, droughts, heatwaves, hurricanes, and fires. But it’s important to keep things in perspective.

There are better and worse ways of managing climate risk. Many investors falsely believe we are transitioning to a world that runs on solar energy, wind power, and batteries. But solar and wind power are unreliable: the sun doesn’t always shine, the wind doesn’t always blow, and batteries are too expensive to store enough energy to power the electrical grid.[4] Efforts to shift to solar and wind power inevitably lead to energy shortfalls and increased energy prices for consumers. Solar and wind are useful for certain niche applications, but they don’t scale well and end up distracting us from more effective ways of reducing climate risk. I wrote more about the problems with solar power in another article: “Solar’s Dirty Secrets.”

Pushing to phase out fossil fuels and nuclear energy without a realistic plan to replace them has resulted in rising energy prices, power blackouts, and fuel shortages in Europe, the United States, and parts of Asia. And it has made people more vulnerable to climate risk by curtailing their access to energy.[5]

Wealthier countries are in general more resilient and better able to adapt to climate risk. The global population grew from 2 billion people in 1900 to 7.7 billion today.[6] Yet deaths due to natural disasters have plummeted over 95% during the last 100 years as the world has gotten wealthier (Figure 2).[7] One way of mitigating the human impact of climate risk is to reduce energy poverty and invest in forms of energy that continue fueling economic growth.

Figure 2: Fewer people have died from natural disasters as the world has grown more wealthy.

Market incentives contribute to supply shortages

The energy sector is currently underinvested because many investors lost money betting on it over the past decade. In the early 2000s, a breakthrough in new horizontal drilling technology led to an oil and gas boom, and investors began pouring money into new exploration. Production started to rise in 2008, and the next seven years marked the fastest increase in oil and gas production in U.S. history. But this boom led to global oversupply, causing prices to crash and investors to lose money and stop investing (Figure 3).

Demand eventually ate up the surplus supply, and energy prices are once again increasing. But investors remain gun-shy: they’re reluctant to pour money back into new exploration and production, and the stock market continues to reward energy companies for paying dividends rather than investing in exploration or innovation. As a result, long-term projects are getting pushed into the future.

Figure 3: Underinvestment in supply contributes to current energy shortages.

The supply squeeze is going to last longer than many investors think. Solar and wind aren’t going to meet our energy needs, and the current lack of investment in the energy sector will contribute to energy shortages and higher prices.

The investment case for natural gas and nuclear energy

All energy sources have tradeoffs. Natural gas and nuclear power are no different. Nevertheless, they rise to the top of the best energy options when you consider the alternatives and their tradeoffs.

Burning coal and oil generates pollution and greenhouse gases.

Solar and wind power are unreliable; they increase energy prices for consumers and don’t scale well.

Hydroelectric dams and geothermal plants can’t be built in all the places people need energy because not all places have suitable water and geothermal sources.

Biofuels require an enormous amount of land, water, and chemicals and cause air pollution.

Nuclear and natural gas are reliable, affordable, and produce low emissions. They’re not perfect. But their shortcomings are more manageable than the alternatives, and their advantages can’t be beat.

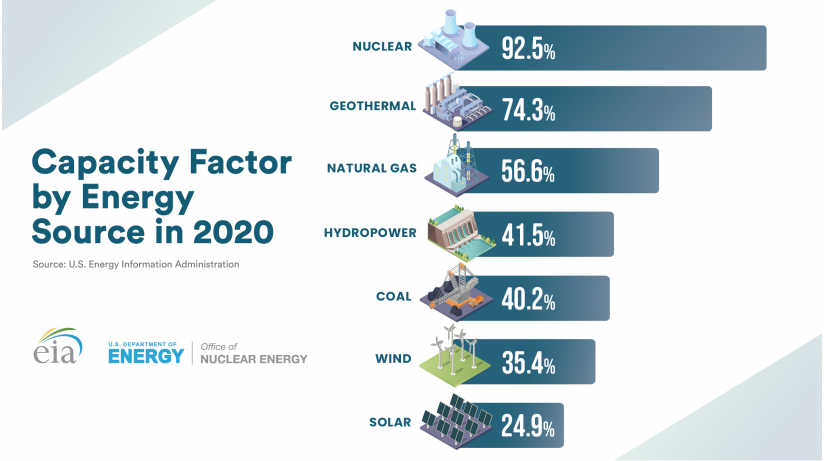

The biggest advantage is that nuclear and natural gas are both extremely reliable sources of power (Figure 4). Nuclear is, in fact, the most reliable of all energy sources.

Figure 4: The capacity factor of a power plant tracks the time it produces maximum power throughout the year.

In addition, both nuclear and natural gas reduce greenhouse gas emissions. Nuclear power plants don’t emit any greenhouse gases or air pollution while operating. And natural gas produces about 50% of the carbon dioxide and just 10% the air pollutants that coal does.

Contrary to what many investors think, the biggest greenhouse gas reductions over the past 15 years haven’t come from increased solar and wind power, but from shifts away from coal and toward natural gas.[8]

Moreover, nuclear and natural gas have the highest power densities of all energy sources, so they require less land to operate than other energy sources. Consequently, both help preserve natural ecosystems.

Natural gas is flexible and helps grid operators ramp power plants up and down quickly to accommodate changes in demand, and it provides an essential backup for intermittent power sources like solar and wind.

In addition, natural gas continues to be essential for heating, cooking, and producing fertilizer, steel, fuel, motor oils, plastics, detergents, cosmetics, and many other products.

The biggest concern with natural gas is that it emits methane, a greenhouse gas. But it’s possible to capture the methane before it escapes and thus decrease the amount released into the atmosphere.

Nuclear is the safest, the most powerful, and the most reliable way to generate electricity. Once the reactors are built, they are relatively cheap to operate. Countries that rely heavily on nuclear power have below-average retail electricity prices.[9] And nuclear plants can operate for 80-100 years if they’re well maintained.[10]

The biggest problem facing nuclear power is lack of will. The public’s misperception about nuclear’s safety is based on irrational fear. People think nuclear power plants are dangerous for the same reason they think airplanes are more dangerous than cars: they’re swayed by emotion rather than the evidence.[11] Just as airplanes are far safer than cars, nuclear is far safer than other energy sources.[12][13] This fear has nevertheless resulted in the E.U. and U.S. having very strict regulatory and financing hurdles that make the process of building nuclear plants slow and expensive.[14] But it doesn’t have to be.

Japan built a nuclear reactor in just over 3 years.[15] France built over 50 nuclear reactors in 15 years and currently gets 70% of its electricity from nuclear power.[16] And China plans to build 150 nuclear power reactors in the next 15 years at about one-third the cost of recent projects in the U.S. and France.[17]

The future of energy

Many investors feel confused by the myriad divergent messages they’re hearing about renewable energy and climate risk. Their uncertainty is why energy stocks are trading at historic lows. But one thing is certain: people are going to continue needing energy. When we weigh the costs and benefits of different energy sources, nuclear and natural gas are the inevitable winners in the energy sector. Their advantages are enormous, and their shortcomings can be managed. In fact, managing the shortcomings creates part of the investment opportunity: developing better, cheaper methods to produce energy.

It’s difficult to find investment opportunities with tremendous financial upside that also advance human flourishing and protect nature. And it’s rare to be positioned so well to capitalize on future growth. Don’t miss out!

[13] Environmental Progress, “Nuclear energy accidents, although rare, have led to fatalities in operators, first responders, and civilians,” Environmentalprogress.com, https://environmentalprogress.org/nuclear-deaths